Every UK crypto investor has a losing position somewhere. A token that went to zero after a rug pull. Coins locked on a collapsed exchange. A wallet with a forgotten seed phrase. A DeFi protocol that got hacked and drained. Crypto losses UK rules are surprisingly generous once you understand them, but most investors either do not claim what they are entitled to, or claim incorrectly and lose the relief entirely.

Every UK crypto investor has a losing position somewhere. A token that went to zero after a rug pull. Coins locked on a collapsed exchange. A wallet with a forgotten seed phrase. A DeFi protocol that got hacked and drained. Crypto losses UK rules are surprisingly generous once you understand them, but most investors either do not claim what they are entitled to, or claim incorrectly and lose the relief entirely.

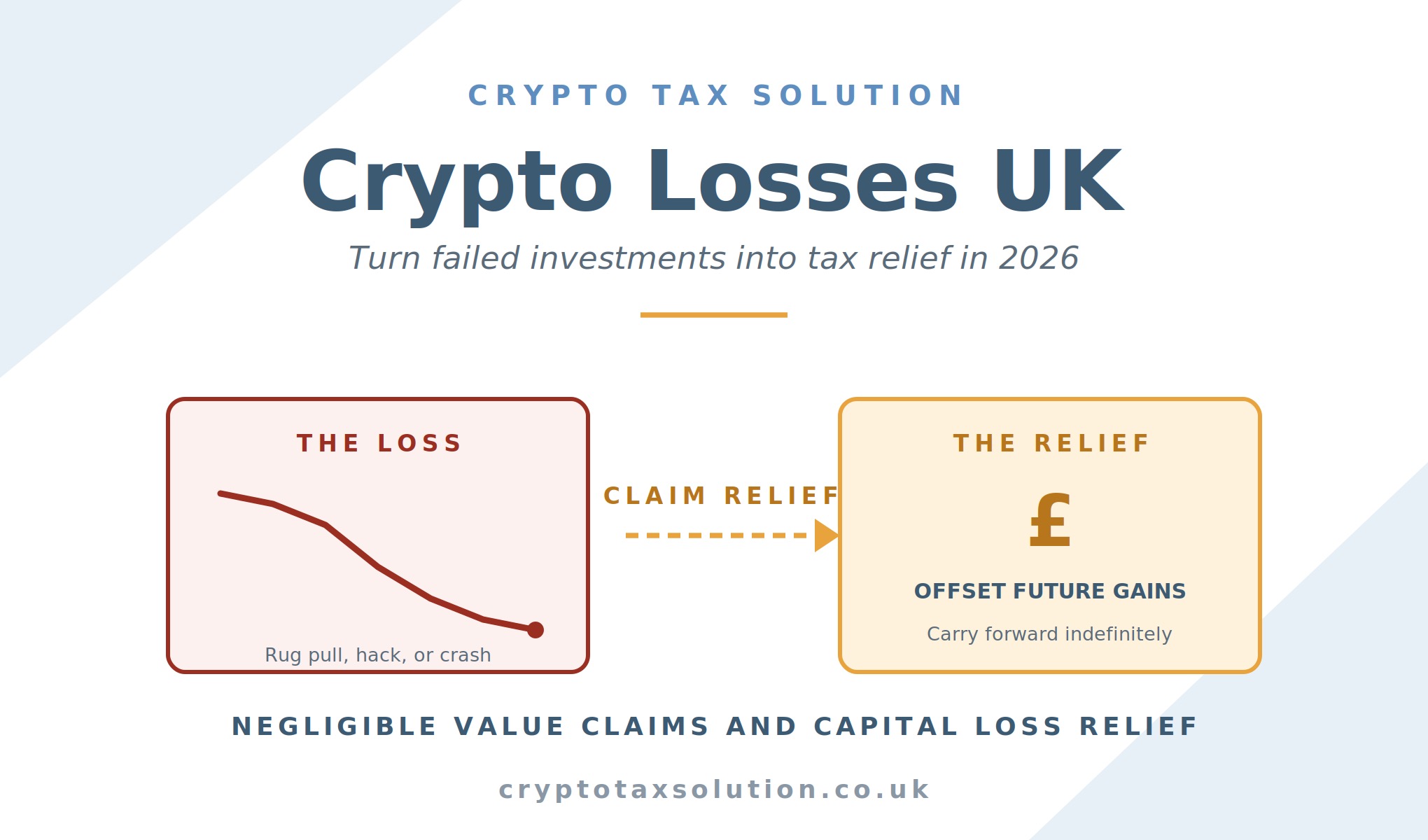

The good news is that HMRC treats crypto losses UK the same way it treats other capital losses. You can offset them against gains, carry them forward, and in some cases claim relief on tokens that are still in your wallet but have become worthless. The rules are technical but the tax saving is real.

This guide explains exactly how crypto losses UK rules work in 2026, the six situations HMRC recognises, how to make a negligible value claim on tokens you still hold, and what to do if you lost crypto to an exchange collapse, a hack, or a lost private key.

The six types of crypto losses HMRC recognises

Not all crypto losses UK investors experience result in the same tax treatment. HMRC recognises six distinct crypto losses UK situations, each with different rules:

- Sold or swapped at a loss: The standard case. You dispose of crypto for less than you paid. The loss is realised at disposal.

- Negligible value tokens still held: The tokens have become essentially worthless but are still in your wallet. A negligible value claim treats them as if disposed of, crystallising the loss without you having to actually sell.

- Lost private keys or seed phrases: The crypto still exists on the blockchain, but you can no longer access it. HMRC’s position is nuanced and requires evidence.

- Stolen crypto (hacks and phishing): Tokens taken from your wallet without your consent. HMRC generally does not treat these as losses because you have not disposed of them.

- Exchange collapses: Crypto held on FTX, Celsius, Voyager, and similar failed platforms. Depends heavily on the specific facts and any recoveries from bankruptcy.

- Rug pulls and scam tokens: Tokens where the project developers exited with the funds and the token is now worthless. Usually treated as negligible value claims.

The treatment matters because it decides when the loss crystallises, what evidence you need, and whether the loss is available at all. Getting the wrong category can mean losing relief you were entitled to.

The basics: standard capital loss relief for crypto

The simplest crypto losses UK case is the one HMRC handles most cleanly. You buy Bitcoin at £30,000 and it drops. Standard capital loss relief applies. Suppose you sell at £20,000, sell it at £20,000, and realise a £10,000 capital loss. Standard capital loss relief rules apply:

- Offset against gains in the same tax year first. Losses reduce your taxable gains before the £3,000 annual exempt amount applies.

- Carry unused losses forward indefinitely. Any losses you cannot use in the current year sit on your record for future use against future gains.

- You cannot offset crypto losses against income. Only against capital gains. This applies to investors. If HMRC classifies you as a financial trader, different rules apply.

- Claim within four years of the tax year end. Losses must be formally claimed on your self-assessment return within four tax years, otherwise they are lost.

The four-year window catches out more investors than any other rule. If you had a loss in 2020/21 and never claimed it on a return, the deadline to claim was 5 April 2025. Any loss not claimed by then is gone. This is why active checking of past-year positions is critical.

Negligible value claims: for tokens still in your wallet

One of the most useful and least understood crypto losses UK rules is the negligible value claim. Most investors miss this entirely. It allows you to crystallise a loss on tokens that have become essentially worthless without actually having to sell them or transfer them.

To make a negligible value claim within the crypto losses UK regime, three conditions must be met:

- The tokens must have become of negligible value. HMRC interprets this strictly. The tokens must be worth so little that they are essentially worthless. Down 90% is not enough. Trading at fractions of a penny with no meaningful liquidity might qualify.

- The tokens must have had value when you acquired them. If they were worthless when you bought them, you never had a gain to lose.

- You must still own them. You are claiming a loss on tokens you still hold, treating the loss as if you had disposed of them.

The claim is made on your self-assessment return. You specify the date the tokens became of negligible value, the amount of the loss, and the tokens involved. HMRC can challenge the valuation and the timing, so evidence matters: dead project websites, delisted exchanges, dead social media, zero trading volume.

You can backdate a negligible value claim by up to two tax years. If tokens became worthless in 2023/24 but you are only claiming now, you can date the claim to 2023/24 or 2024/25, which may be useful if that year had gains to offset.

Crypto losses UK from exchange collapses

Exchange collapses caused some of the largest crypto losses UK investors have ever seen. Understanding the crypto losses UK rules for failed platforms matters more here than in almost any other loss scenario. FTX, Celsius, Voyager, BlockFi, and others took client funds into bankruptcy. HMRC treatment is more complex than a simple negligible value claim.

The core question for these crypto losses UK is whether you still have a legal right to any of the tokens. Until bankruptcy proceedings conclude, you typically have a claim against the estate for some percentage recovery. That claim is itself an asset, even if the underlying tokens are not accessible.

The practical position for most exchange collapse crypto losses UK investors is:

- You cannot claim the full loss immediately. Until the bankruptcy process determines your recovery, the actual loss amount is not fixed.

- Interim distributions reduce your loss. If you receive a partial recovery, that amount comes off your loss claim.

- Final loss is crystallised when the claim concludes. Once the bankruptcy is settled and no further recovery is possible, the loss is finalised.

- Some UK investors have made crypto losses UK claims sooner via negligible value. Particularly where recovery is expected to be minimal or where the bankruptcy is taking years. HMRC has accepted this in some cases but requires strong evidence.

Exchange collapse losses genuinely need professional advice. The interaction with the recovery process, timing of the claim, and evidence requirements make DIY claims risky.

Lost crypto: keys, hacks, and stolen wallets

Lost crypto is where the crypto losses UK rules get most technical. HMRC treats different situations very differently.

Lost private keys or seed phrases. HMRC’s stated position is that if you have permanently lost access to your crypto because you cannot recover your keys, you may be able to make a negligible value claim. But the burden of proof is on you, and “I forgot my password” is not enough. You need to demonstrate that the loss is genuine and permanent, and that recovery is not reasonably possible.

Hacked or stolen wallets. If someone drains your wallet, HMRC generally does not treat this as a loss for CGT purposes. HMRC’s position on crypto losses UK from theft is that you still own the tokens, someone else just has them. This position has been criticised as unfair, but it is the current HMRC line.

Phishing and scam transfers. Where you were tricked into signing a transaction that transferred your crypto to a scammer, HMRC’s position is similar to theft. The disposal was voluntary in a technical sense, even if you were deceived.

Crypto losses UK from hacks and lost keys are areas where the law and HMRC guidance are still developing. Cases have been made both ways at tribunal. If you have lost significant amounts through hacks or scams, specialist advice is essential.

The 30-day bed and breakfast rule can disallow crypto losses UK claims

One rule that catches active traders is the 30-day bed and breakfast rule. If you sell crypto at a loss and buy the same crypto back within 30 days, the loss is disallowed. Instead, the new acquisition cost matches the disposal cost, effectively cancelling the loss.

Applied to crypto losses UK claims, this rule stops investors from crystallising a paper loss for tax purposes and immediately re-establishing the position. It is a specific anti-avoidance rule and it is enforced.

For crypto losses UK investors who trade actively, the 30-day rule is a real trap. Selling ETH at a loss on 1 April, buying it back on 5 April to catch a rebound, and claiming the loss on your tax return will not work. The loss is disallowed and your new ETH position simply carries the old cost basis.

The way around it, if you want to realise the loss, is to either wait 31 days before repurchasing, or purchase a different token entirely. Some investors use the interim period to hold cash or a different crypto to maintain some market exposure.

How to record and claim crypto losses UK on self-assessment

Even the cleanest crypto losses UK claim needs proper documentation. HMRC increasingly reviews crypto positions and disallows claims that lack evidence. The minimum you need for each loss:

- Acquisition record: Date acquired, cost in GBP at the time (including any fees), and the token in question.

- Disposal or negligible value record: Date of disposal or the date you claim the value became negligible, and the sale proceeds (if any) or valuation.

- Evidence supporting the loss: For a sale, exchange statements. For a negligible value claim, evidence that the token is genuinely worthless. For lost keys, contemporaneous records of the loss.

- Calculation of the loss: Cost minus proceeds, adjusted for any allowable expenses.

The loss is reported on the capital gains supplementary pages of your self-assessment return (SA108). You need to complete the loss box and provide a supporting computation. HMRC does not require you to attach every transaction, but you must be able to produce the records if asked.

For CARF-era reporting of crypto losses UK claims (from January 2026), HMRC will independently know about many of your exchange transactions. Any inconsistency between your loss claim and their data will invite an enquiry.

Frequently Asked Questions

Can I claim crypto losses UK against my salary income?

No, not as an ordinary investor. Crypto losses can only be offset against capital gains, not against income tax on your salary or self-employment profits. The exception is if HMRC classifies your crypto activity as a financial trade, in which case different rules apply and losses can offset trading income.

How long can I carry forward crypto losses UK?

Indefinitely, provided you claim the loss within four years of the end of the tax year in which it arose. Once claimed, the loss sits on your capital losses record and can be used against any capital gain in any future tax year until fully absorbed.

Can I claim a loss on crypto stuck on a failed exchange?

Not automatically, and usually not in full until the bankruptcy process concludes. Interim negligible value claims are possible in some cases where recovery is expected to be minimal, but require strong evidence. Specialist advice is strongly recommended for exchange collapse losses.

Does HMRC accept negligible value claims on scam tokens?

Yes, in most cases. If a token you invested in turns out to be a rug pull or scam, and the token is now essentially worthless, a negligible value claim is normally available. Evidence of the project’s failure (dead website, delisted exchanges, no trading volume) supports the claim.

What if I lost access to my crypto wallet years ago?

You may be able to make a negligible value claim, backdated up to two tax years. Beyond that, unclaimed losses from prior years may still be claimable if you never used them, but this is complex and specialist advice is worth taking. Contemporaneous evidence of the loss significantly strengthens the claim.

Crypto losses UK: get the right advice before you claim

Crypto losses UK claims are one of the most valuable reliefs in UK crypto tax, and one of the most complex. The relief is real, but the rules are technical, the evidence requirements are demanding, and the interaction with the 30-day rule, exchange bankruptcies, and negligible value claims catches out most investors trying to file alone.

At Crypto Tax Solution we help UK crypto investors identify and claim every loss they are entitled to, in the correct tax year, with the evidence to withstand HMRC scrutiny. Get in touch for a review of your loss position and the reliefs you may be missing. For HMRC’s official guidance, see the Cryptoassets Manual.