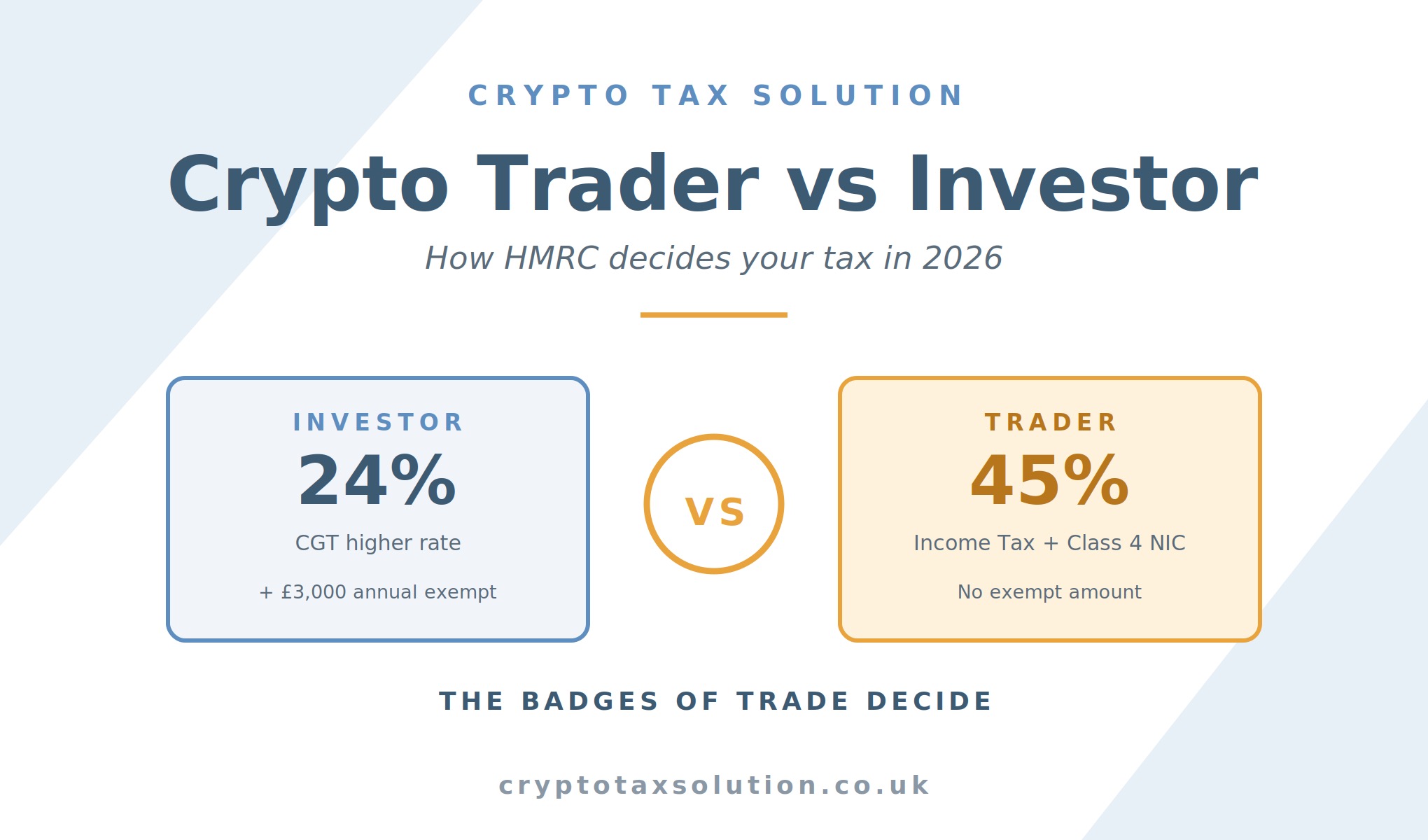

The crypto trader vs investor UK question is the single most expensive distinction in UK crypto tax. Get it wrong and the difference can be tens of thousands of pounds in tax on the same trading profits. Most UK crypto holders are investors and pay Capital Gains Tax at 18% or 24%. A smaller group are treated by HMRC as financial traders and pay Income Tax at up to 45%, plus Class 4 National Insurance on top.

The crypto trader vs investor UK question is the single most expensive distinction in UK crypto tax. Get it wrong and the difference can be tens of thousands of pounds in tax on the same trading profits. Most UK crypto holders are investors and pay Capital Gains Tax at 18% or 24%. A smaller group are treated by HMRC as financial traders and pay Income Tax at up to 45%, plus Class 4 National Insurance on top.

The problem is that there is no bright-line test. HMRC decides the crypto trader vs investor UK question by applying a centuries-old set of principles called the “badges of trade”, originally developed for buying and selling physical goods and now reluctantly applied to digital assets. Most people who think they are investors are correct. A minority who are very active are at real risk of being reclassified.

This guide explains exactly how the crypto trader vs investor UK distinction works in 2026, the badges of trade HMRC actually applies, the warning signs that you might be exposed, and what to do if you think your activity has crossed the line.

Why HMRC distinguishes between traders and investors

The reason the crypto trader vs investor UK question matters is straightforward. The two categories sit in completely different parts of the tax system, and the difference in cash tax can be eye-watering.

On the investor side of the crypto trader vs investor UK line, an investor buys cryptoassets hoping they will rise in value over time. When they sell, swap or otherwise dispose of those assets, any gain is taxed as a capital gain. For 2026/27, CGT rates are 18% (basic rate) and 24% (higher rate), with a £3,000 annual exempt amount. Losses can be carried forward and offset against future capital gains.

A trader is treated as running a financial business. Profits are taxed as trading income at standard Income Tax rates (20%, 40% or 45%), and Class 4 NIC applies at 6% between £12,570 and £50,270, then 2% above. There is no annual exempt amount equivalent to the £3,000 CGT allowance. The starting position is significantly more expensive.

So the crypto trader vs investor UK question is essentially: which set of rules apply to me? The answer determines whether your 2026/27 tax bill is calculated using one regime or the other.

The default position: most UK crypto users are investors

HMRC’s cryptoassets manual is unambiguous on this point. The default treatment for individuals is investor status, taxed under CGT rules. HMRC explicitly states that only in exceptional circumstances would it expect individuals to buy and sell cryptoassets with such frequency, organisation and sophistication that the activity amounts to a financial trade.

This is genuinely good news for most UK crypto holders. Buying Bitcoin or Ethereum and holding it long term, occasionally rebalancing, or even active trading on a part-time hobby basis, will normally fall on the investor side of the crypto trader vs investor UK line.

The trader classification is reserved for people whose activity looks less like investing and more like running a business. The bar is high, but it is not infinite. Active day traders with high transaction volumes, leverage, and systematic methods can and do get caught.

The badges of trade: how HMRC actually decides

When HMRC has to make a crypto trader vs investor UK call, it applies the “badges of trade” framework. These badges are the foundation of every crypto trader vs investor UK enquiry. They are nine factors derived from case law, set out in HMRC’s Business Income Manual. No single badge is decisive. HMRC looks at the picture as a whole.

Applied to crypto activity, the nine badges look like this:

- Subject matter: Cryptoassets are typically held for investment rather than personal use, which tilts toward investor status by default.

- Frequency of transactions: A handful of trades a year looks investor. Hundreds of trades a month looks like a trade.

- Length of ownership: Long holding periods suggest investment. Holding assets for minutes or hours suggests trading.

- Supplementary work: Active research, technical analysis, custom bots, paid signals services, all suggest organised trading activity.

- Circumstances of sale: Forced sales (urgent need for cash) suggest investment. Systematic profit-taking on signals suggests trade.

- Motive (intention to make profit): Critical badge. If acquired with intent to sell at profit in the short term, that points to trading. Long-term capital appreciation points to investing.

- Method of acquisition: Buying for cash from your own funds suggests investing. Buying with leverage or borrowed money suggests a trading operation.

- Method of finance: Trading on margin, using derivatives, hedging, all push toward trader classification.

- Existence of a similar trade: If you already trade in shares, FX or other financial instruments as a profession, that activity bleeds into your crypto activity for the crypto trader vs investor UK assessment.

HMRC weighs these together. A picture of high frequency + leverage + systematic methods + short holdings + clear short-term profit motive starts to look very different from a picture of someone buying ETH every payday and holding it.

Crypto trader vs investor UK: red flags HMRC looks for

Some patterns dramatically increase the chance of being reclassified as a trader. If several of these apply to you, the crypto trader vs investor UK question needs professional review.

- Hundreds or thousands of transactions per year, particularly across short timeframes.

- Trading on margin or with leverage on platforms like Bybit, Binance Futures, or dYdX.

- Use of automated bots, copy-trading services, or algorithmic strategies.

- Holdings denominated in stablecoins that are frequently rotated between assets, suggesting tactical trading rather than long-term conviction.

- Detailed records of entry and exit points, profit-loss tracking, and systematic strategies.

- Significant time spent daily on analysis, monitoring, and execution.

- Crypto activity that is your primary source of income, even if you have a day job.

- Use of derivative products like perpetual futures or options as a core activity rather than occasional hedging.

None of these in isolation makes you a trader. Several of them together, sustained over time, makes the crypto trader vs investor UK assessment a live question that HMRC could revisit.

Worked example: investor vs trader treatment of a £20,000 profit

To make the crypto trader vs investor UK distinction concrete in pounds, let’s run the same £20,000 profit through both regimes for 2026/27. Assume the individual is already a higher-rate taxpayer earning £70,000 from a salaried job.

Scenario A: investor treatment (CGT).

- Gross gain: £20,000.

- Less annual exempt amount: £3,000.

- Taxable gain: £17,000.

- CGT at 24% (higher rate): £4,080.

- Total tax: £4,080.

Scenario B: trader treatment (Income Tax + NIC).

- Gross profit: £20,000 added to other income.

- Income Tax at 40% higher rate: £8,000.

- Class 4 NIC at 2% (above £50,270): £400.

- Total tax: £8,400.

The difference is £4,320 on the same £20,000 profit. Multiply that across years of active trading and the crypto trader vs investor UK question becomes one of the largest tax decisions a UK crypto holder can face.

And if the crypto trader vs investor UK question lands the individual at additional rate (45%) on profits pushing them over £125,140, the tax bill rises higher still. Trader treatment is rarely the cheaper outcome.

Crypto trader vs investor UK: National Insurance most people miss

The headline rate difference of 40% versus 24% gets the attention, but trader classification also brings National Insurance into scope. Investors pay no NIC on capital gains. Traders pay Class 4 NIC at 6% on profits between £12,570 and £50,270, then 2% above.

A self-employed trader earning £50,000 of net trading profits in 2026/27 would owe roughly £2,260 of Class 4 NIC on top of Income Tax, all of which is invisible until the moment HMRC reclassifies the activity.

Class 2 NIC was abolished for self-employed traders from April 2024, so there is no longer a small flat-rate charge. Class 4 remains, and for the crypto trader vs investor UK question it materially worsens the trader outcome.

How CARF changes the crypto trader vs investor UK question

From 1 January 2026, the Crypto-Asset Reporting Framework requires UK exchanges to report transaction data to HMRC. See our full CARF guide for the detail. The practical impact on the crypto trader vs investor UK question is significant.

Until now, HMRC’s main visibility into your trading patterns came from your own Self Assessment return. Under CARF, exchanges report transaction counts, volumes and patterns directly. HMRC can now see, on a single screen, that you completed 4,000 trades last year across three exchanges, with average holding periods of 90 minutes. That data invites a crypto trader vs investor UK review even where the taxpayer believes they are an investor.

The upshot: high-frequency UK crypto activity that was previously invisible to HMRC is now reported by default. Voluntary review of your own classification is increasingly important.

How to manage the crypto trader vs investor UK risk

If your activity has grown to the point where the crypto trader vs investor UK question is genuinely live, there are practical steps to take.

- Honestly audit your trading patterns. Pull a transaction count, average holding period and total volume across all exchanges and wallets for the last two tax years.

- Document your investment thesis. Long-form notes on why you hold specific assets, written contemporaneously, support investor classification.

- Reduce leverage and derivatives use if you want to stay clearly on the investor side. Margin trading is one of the strongest pointers toward trader status.

- Avoid bot-based or algorithmic strategies unless you are prepared to be classified as a trader and pay accordingly.

- Take advice early. If HMRC challenges you, the time to have built the evidence trail is years before, not the day the letter arrives.

- Consider voluntary disclosure if past activity could be reclassified as trading. Penalties for unprompted disclosure are materially lower than for prompted ones.

For more on how HMRC is using CARF data, see our coverage of the HMRC crypto nudge letter wave and what to do if you receive one.

Frequently Asked Questions

How does HMRC decide if I am a crypto trader or investor?

HMRC applies the badges of trade, a set of nine factors from case law, to the whole picture of your activity. Frequency, holding periods, use of leverage, motive and supplementary work all matter. No single factor is decisive. Most UK crypto users are investors under this test.

How many crypto trades make me a trader for tax?

There is no specific transaction threshold in the crypto trader vs investor UK rules. HMRC looks at the totality of the activity. As a guide, casual investors typically run from a handful to maybe a hundred trades a year. Activity at thousands of trades a year, especially with leverage or bots, starts to look like a trade.

Can I choose to be taxed as a crypto trader?

No. The crypto trader vs investor UK classification is decided by HMRC based on the facts, not by election. You cannot choose income tax treatment if your activity does not meet the badges of trade, and you cannot choose CGT treatment if your activity clearly does.

Is being classified as a crypto trader ever a good thing?

Rarely. Trader treatment usually produces a higher tax bill because of Income Tax rates plus Class 4 NIC. The only common scenarios where trader status is advantageous is where the individual has large trading losses they could offset against other income, which CGT loss rules would not allow.

What if HMRC reclassifies me as a trader retrospectively?

This is the real risk. HMRC can open enquiries into past tax years and reassess on a trader basis, with the higher tax bill, interest and potentially penalties. CARF data starting in 2026 makes retrospective enquiries more likely. Voluntary disclosure before HMRC contacts you is almost always materially cheaper.

Crypto trader vs investor UK: get expert advice

The crypto trader vs investor UK question is one of the highest-stakes decisions in UK crypto tax. The badges of trade are technical, the case law is fact-specific, and the financial difference between the two classifications is enormous. Getting it wrong, in either direction, is expensive.

At Crypto Tax Solution we help active UK crypto users assess their crypto trader vs investor UK exposure, build the evidence trail to support their preferred classification, and respond to HMRC enquiries when they arrive. Get in touch today for a confidential review of where you stand.