DeFi tax UK rules are the most misunderstood corner of UK crypto taxation, and the most expensive to get wrong. Depositing tokens into Aave, providing liquidity on Uniswap, or locking collateral for a loan can each be a taxable disposal under current HMRC rules, even though you never sold anything and never received a penny of cash. The industry calls this the “dry tax” problem, and thousands of UK DeFi users have unknowingly triggered it.

DeFi tax UK rules are the most misunderstood corner of UK crypto taxation, and the most expensive to get wrong. Depositing tokens into Aave, providing liquidity on Uniswap, or locking collateral for a loan can each be a taxable disposal under current HMRC rules, even though you never sold anything and never received a penny of cash. The industry calls this the “dry tax” problem, and thousands of UK DeFi users have unknowingly triggered it.

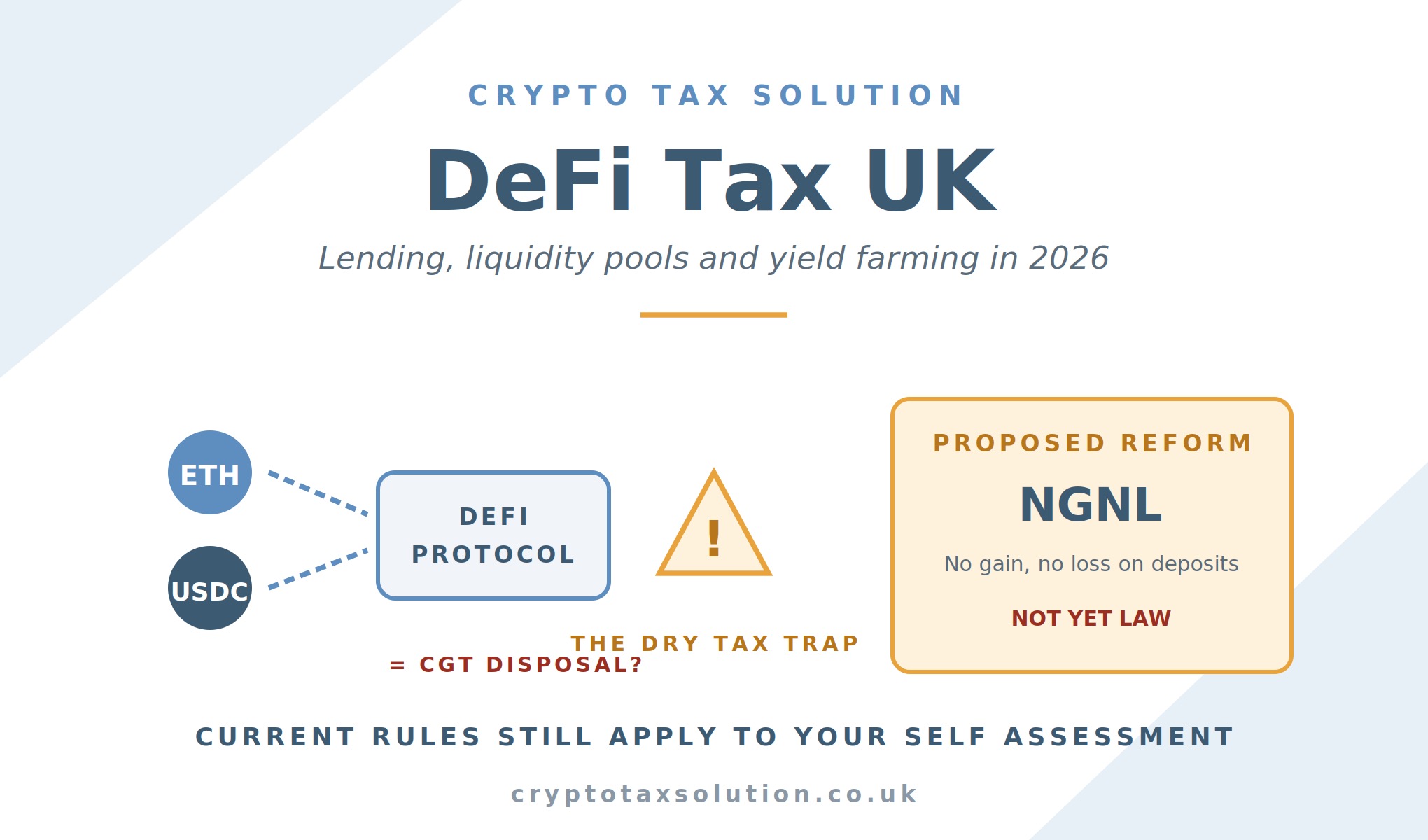

The DeFi tax UK rules are changing. HMRC has proposed a “no gain, no loss” framework that would defer tax until you economically exit a position, and the consultation outcome published in late 2025 shows broad support. But here is the part most DeFi users miss: that framework is a proposal, not law. For your current Self Assessment, the old rules still apply in full.

This guide explains how DeFi tax UK rules actually work in 2026, when a deposit becomes a disposal, how lending returns and liquidity pool rewards are taxed, what the proposed NGNL rules would change, and what to do about past DeFi activity you never reported.

The core problem: DeFi deposits can be disposals

The starting point for DeFi tax UK analysis is HMRC’s cryptoassets manual, which treats a transfer of tokens as a disposal for Capital Gains Tax whenever beneficial ownership changes. That single principle drives almost every difficult DeFi outcome:

- Lending tokens through a protocol: If the protocol (or borrower) can deal with your tokens freely, beneficial ownership has probably passed. That is a disposal at market value, even though you expect the same tokens back.

- Providing liquidity to an AMM pool: You deposit two tokens and receive LP tokens in exchange. HMRC’s view is that you have disposed of the deposited tokens and acquired a new asset (the LP tokens).

- Posting collateral for a loan: Depending on the protocol’s terms, locking collateral can also transfer beneficial ownership and trigger a disposal.

- Wrapping tokens: Converting ETH to wETH or BTC to wBTC involves exchanging one asset for another, which HMRC generally treats as a disposal.

Each of these events crystallises a gain or loss measured against your original acquisition cost, payable in cash, even though the transaction gave you no cash. That is the dry tax charge at the heart of the DeFi tax UK problem.

When is a DeFi deposit NOT a disposal?

Not every interaction with a protocol triggers DeFi tax UK liability. The DeFi tax UK analysis is fact-specific and turns on the terms of the arrangement:

- No change in beneficial ownership: If the protocol cannot deal with your tokens as its own, and you retain the right to the same tokens back, ownership may not have passed. Some custody-style arrangements fall on this side of the line.

- Transfers between your own wallets: Moving tokens from your exchange account to your own MetaMask wallet is not a disposal. You still own them.

- Some collateral arrangements: Where the terms restrict the platform from dealing with your collateral, the deposit may not be a disposal.

The dividing line is contractual and technical: what do the protocol’s terms actually say, and what does the smart contract actually do with your tokens? Two protocols offering identical yields can produce completely different DeFi tax UK outcomes based on their mechanics. This is exactly the kind of analysis where specialist review pays for itself.

How DeFi returns are taxed: income or capital?

The second half of the DeFi tax UK puzzle is how DeFi tax UK rules treat the returns: lending interest, liquidity pool fees, yield farming rewards, incentive tokens. HMRC rules out treating any of these as interest (crypto is not money), so each return must be characterised as either income or capital based on the facts.

The factors HMRC weighs:

- Known in advance vs speculative: A fixed 5% APY agreed upfront points to income. A return dependent on pool performance points to capital.

- Periodic vs one-off: Rewards paid daily or weekly look like income. A single settlement at exit looks more like capital.

- Service vs growth: Returns earned for providing a service to the platform (lending, liquidity provision) tend to be income. Returns from the capital growth of an asset you hold tend to be capital.

Most routine DeFi lending and liquidity rewards end up taxed as miscellaneous income at their sterling value on the date of receipt. That value then becomes the base cost for a future CGT disposal of the reward tokens. Income tax rates up to 45% versus CGT at 24% make this characterisation question worth real money, and it is decided by the arrangement’s facts, not by what you would prefer.

Liquidity pools: the hardest DeFi tax UK case

Automated market maker pools produce the most complex DeFi tax UK calculations of any activity, and they are where most DeFi tax UK errors happen. A single Uniswap position involves:

- Entry: Disposal of both deposited tokens at market value, plus acquisition of LP tokens as a new asset.

- During: Fee income accruing inside the pool, plus impermanent loss or gain silently changing the composition of what you will eventually withdraw.

- Exit: Disposal of the LP tokens, plus acquisition of whatever token amounts come back, which will rarely match what you deposited.

Each leg needs a sterling valuation at the transaction date. An active liquidity provider rebalancing across pools can generate hundreds of taxable events per year, each requiring a market-value computation. Without software and specialist support, accurate reporting is close to impossible, which is precisely why HMRC has accepted the current rules create a disproportionate burden.

The proposed no gain, no loss rules: what changes and when

After years of criticism of the DeFi tax UK regime, HMRC consulted on reform and published its summary of responses in late 2025. The direction of travel is a “no gain, no loss” (NGNL) framework for DeFi tax UK purposes:

- Deposits into lending and liquidity positions would no longer trigger CGT. The transfer in would be treated as no gain, no loss, provided you retain the right to reclaim equivalent tokens.

- Tax would arise on economic disposal only: selling, swapping outside the protocol, or cashing out to fiat.

- AMM pools would use a “reference quantity” approach: comparing what you withdraw against what you contributed, taxing only the excess as gain (or shortfall as loss).

- Returns would still be taxed as income at receipt. NGNL changes the disposal timing, not the treatment of rewards.

The critical caveat: none of this is law yet. No draft legislation has been published. Until it is, DeFi tax UK compliance means applying the current disposal rules in full. Anyone filing on the basis of the proposed rules is filing incorrectly, and CARF data now gives HMRC the visibility to notice.

CARF and DeFi: your activity is now visible

From 1 January 2026, the Crypto-Asset Reporting Framework requires crypto service providers to report UK users’ transaction data to HMRC. See our full CARF guide for the detail.

For anyone with DeFi tax UK exposure the practical consequence is sharp: HMRC can increasingly see the on-ramps and off-ramps around your DeFi activity, even where pure on-chain activity is harder to observe. Large transfers out to self-custody, followed by large returns to an exchange months later, invite the obvious question of what happened in between. Unreported DeFi tax UK liabilities from earlier years are far more likely to surface now than they were even a year ago.

If you have historic DeFi activity you never reported, a voluntary disclosure before HMRC contacts you attracts materially lower penalties than a prompted one. Our HMRC nudge letter guide covers what happens once HMRC makes the first move.

Practical steps for DeFi users in 2026

- Map your DeFi tax UK positions. List every protocol, pool and lending arrangement you have entered, with dates and token amounts. This is the raw material for any accurate DeFi tax UK computation.

- Use tracking software, but do not trust it blindly. Crypto tax software handles exchanges well and DeFi inconsistently. LP entries, wrapped tokens and reward claims are the usual failure points. Review the output.

- Keep the terms. Screenshot or archive the protocol terms for significant positions. The disposal question turns on those terms, and protocols change or disappear.

- Record sterling values at every transaction date. Both disposals and income receipts need GBP valuations at the time, not at year end.

- Review historic DeFi tax UK years now. The four-year window for correcting past returns and claiming losses is running. CARF makes waiting a strategy with a shortening shelf life.

- Take advice before large entries or exits. The difference between entering a position on 4 April versus 6 April, or choosing one protocol structure over another, can move a five-figure tax outcome.

Frequently Asked Questions

Is depositing crypto into a DeFi protocol taxable in the UK?

Often yes, under current rules. If beneficial ownership of the tokens passes to the protocol or borrower, the deposit is a disposal for CGT at market value, even though you receive no cash. Whether ownership passes depends on the protocol’s terms. Proposed no gain, no loss rules would change this, but they are not yet law.

How is DeFi lending interest taxed in the UK?

Returns from DeFi lending cannot be interest for tax purposes because crypto is not money. Most lending returns are taxed as miscellaneous income at their sterling value on receipt, with that value forming the base cost for a later CGT disposal. Capital treatment is possible where the return depends on capital growth rather than a service.

Are liquidity pool tokens taxable?

Receiving LP tokens usually follows a disposal of the tokens you deposited, under current DeFi tax UK rules. The LP tokens are a new asset with their own base cost. Withdrawing liquidity is a further disposal of the LP tokens. Pool rewards are generally income at receipt.

When do the new no gain, no loss DeFi rules start?

No start date exists. HMRC published its consultation outcome in late 2025 showing support for an NGNL framework, but no draft legislation has been published. Until legislation passes, the current disposal-based rules apply to all DeFi tax UK reporting.

What if I never reported my old DeFi transactions?

Review them now and consider a voluntary disclosure. Unprompted disclosures attract significantly lower penalties than prompted ones, and CARF reporting from January 2026 makes historic activity far more visible to HMRC. Losses from failed positions may also be claimable, which can reduce what you owe.

DeFi tax UK: get specialist help before HMRC asks

DeFi tax UK is the most technically demanding area of UK crypto taxation. The disposal analysis is fact-specific, the income-versus-capital question is worth real money, the software gets it wrong more often than users realise, and the rules themselves are mid-transition between the current regime and the proposed NGNL framework.

At Crypto Tax Solution we specialise in exactly this territory: reconstructing DeFi transaction histories, applying the correct disposal and income treatment, correcting past returns, and managing voluntary disclosures before HMRC comes calling. Get in touch for a confidential review of your DeFi position. For HMRC’s official guidance, see the Cryptoassets Manual.